Explained: Banking on SaaS-driven Enterprise Fraud Management

Image courtesy: rawpixel on Freepik

Image courtesy: rawpixel on Freepik

A bank’s risk and compliance leadership are faced with a wide spectrum of challenges when it comes to effective real-time Enterprise Fraud Management, including –

In an era where digital transactions have become the norm, ensuring the security of financial systems has become a top priority for banks worldwide. The rising threat of fraudulent activities poses significant challenges to the banking industry. To combat this menace effectively, banks must adopt innovative solutions that not only protect their customers’ financial interests but also streamline their operations. One promising direction is adopting an Enterprise Fraud Management (EFM) system in Software-as-a-Service (SaaS) mode.

Let’s explore why banks should embrace this progressive technology to fortify their anti-fraud defences and stay ahead of fraudsters.

1. Enhanced Fraud Detection

The foremost benefit of implementing an EFM solution in SaaS mode is its ability to significantly enhance fraud detection capabilities. Conventional fraud management systems often rely on rule-based approaches, which can be rigid and unable to keep up with evolving fraud tactics. However, an EFM system employs advanced analytics and machine learning algorithms to detect patterns, anomalies, and behavioural changes in real-time. By analysing vast amounts of data from multiple sources, including transactions, customer profiles, and external data feeds, an EFM solution can accurately identify potentially fraudulent activities and trigger alerts, allowing banks to take swift preventive measures.

2. Scalability and Flexibility

On-prem solutions typically plan for their best-guess peak load while utilizing only 40-50% of the work load. A sudden surge in transaction volumes (attributed to various factors) leads to tactical, reactive compromises which results in either delayed fraud detection coupled with the risk of losses to the fraud or a plunge in customer experience which impacts the bank’s brand value.

The SaaS model offers banks unparalleled scalability and flexibility when it comes to deploying an EFM solution. Rather than investing heavily in hardware infrastructure and software licenses, banks can leverage the cloud-based nature of SaaS to scale their fraud management capabilities as per their requirements. With a SaaS-based EFM system, banks can seamlessly handle increasing transaction volumes and adapt to changing fraud patterns without compromising system performance. Moreover, the flexibility of the SaaS model allows for easy integration with existing banking systems, reducing the implementation time and cost involved in deploying a new solution.

3. Real-time Monitoring and Response

Fraudsters are constantly evolving their techniques, necessitating a proactive and real-time response from banks. An EFM solution in SaaS mode empowers banks to monitor transactions and detect potential fraud in real-time. By leveraging advanced algorithms and machine learning, banks can identify suspicious activities as they occur, triggering immediate alerts to the appropriate teams for investigation and response. The ability to take swift action against fraudulent transactions can significantly reduce the financial losses incurred by banks and protect the interests of their customers.

4. Comprehensive Risk Assessment

An EFM solution provides banks with a holistic view of risk by aggregating and analysing data from multiple sources. By combining transactional data, customer behaviour, device information, and external data feeds, banks can gain valuable insights into potential vulnerabilities and risk factors. This comprehensive risk assessment allows banks to implement proactive measures and enhance their fraud prevention strategies. Moreover, the continuous monitoring and analysis of data enables banks to adapt their risk models and rules in real-time, ensuring they stay ahead of emerging fraud trends.

5. Cost-effectiveness and Operational Efficiency

Adopting an EFM solution in SaaS mode offers banks significant cost savings and operational efficiencies. The cloud-based infrastructure eliminates the need for large upfront investments in hardware and software licenses while enhancing the capability to meet sudden or planned surge of transaction volumes. Additionally, the SaaS model provides automatic software updates, reducing the burden on banks’ IT departments. By outsourcing infrastructure management and maintenance to the EFM solution provider, banks can focus their resources on core banking activities. The scalability and flexibility of the SaaS model also enables banks to optimize resource allocation and improve operational efficiency.

6. Collaboration and Knowledge Sharing

Fraud is a global problem and banks can benefit greatly from collaborative efforts and knowledge sharing. A SaaS-based EFM solution facilitates information sharing and collaboration among banks. By anonymizing and aggregating data across multiple banks, the solution provider can identify fraud patterns and trends that may not be evident within a single institution. Banks can benefit from collective intelligence, gaining insights into new fraud techniques and preventive measures. This collaborative approach can significantly enhance the effectiveness of fraud management and help banks stay ahead of fraudsters.

As the threat of fraud continues to evolve in an age of fast payments, banks must embrace innovative solutions to safeguard their customers’ financial interests. The adoption of an EFM solution in SaaS mode offers banks enhanced fraud detection capabilities, scalability, flexibility, real-time monitoring, comprehensive risk assessment, cost-effectiveness and collaborative knowledge sharing. By leveraging advanced analytics and machine learning algorithms, banks can detect and prevent fraud in real-time, reducing financial losses and protecting their reputation. With the ever-increasing emphasis on secure financial transactions, the time has come to invest in an EFM solution in SaaS mode to stay ahead in the battle against fraud.

(Sequel to the 2-part blog on improving Customer Lifecycle Management in financial institutions)

Image courtesy: @tawatchai07 on Freepik

Image courtesy: @tawatchai07 on Freepik

‘Well begun is half done’

– Aristotle

In the prequel, we saw how financial institutions can initiate a streamlined CDD-led customer onboarding experience.

Let us now see what it takes to manage what lies ahead.

By thinking more strategically about the customer lifecycle journey – from targeting to acquisition to servicing and developing – and making smarter use of advanced data, analytics and with help from technology, financial institutions can diligently improve customer experience and reduce attrition.

Most FIs are already interpreting the customer’s internet banking and mobile banking behaviour to provide more hyper-personalized services. Leveraging customer transactions and interactions in real-time help make precise ‘segment of one’ cross-sell / upsell recommendations.

To build better relationships, some FIs are also sourcing alternative data, for e.g., customer payment histories for mobile phones, utilities, even cable TV. This data augments traditional credit data with more dimensions to spend behaviours.

When combined with credit data, alternative data can also be a good indicator of the risk potential of customers. In most cases, a reliable risk score for retail banking can be successful in determining account risk. The score can also help identify applicants who might otherwise be turned down, but who have low risk, based on their payment history from alternative data.

By viewing risk scoring from a fraud prevention perspective, FIs can go beyond assessing the viability of new customers and begin addressing dormant or evolving fraud such as ATOs and bust-outs (where seemingly good customers max out available credit before vanishing). Specialized financial crime risk management solutions help identify suspicious activities and potential fraud patterns that are at play in other institutions, and deliver that information in real-time.

These solutions also help FIs maximize revenue and margin at every step along the customer lifecycle, from acquisition to upsell / cross-sell to loyalty / retention to debt management – all while maintaining continuous and stringent due diligence.

A good CLM-enabling solution will help continuously analyse customer behaviours and needs, determine the right objectives (acquisition or retention), and identify ideal ways of targeting them. Specifically, a good solution will –

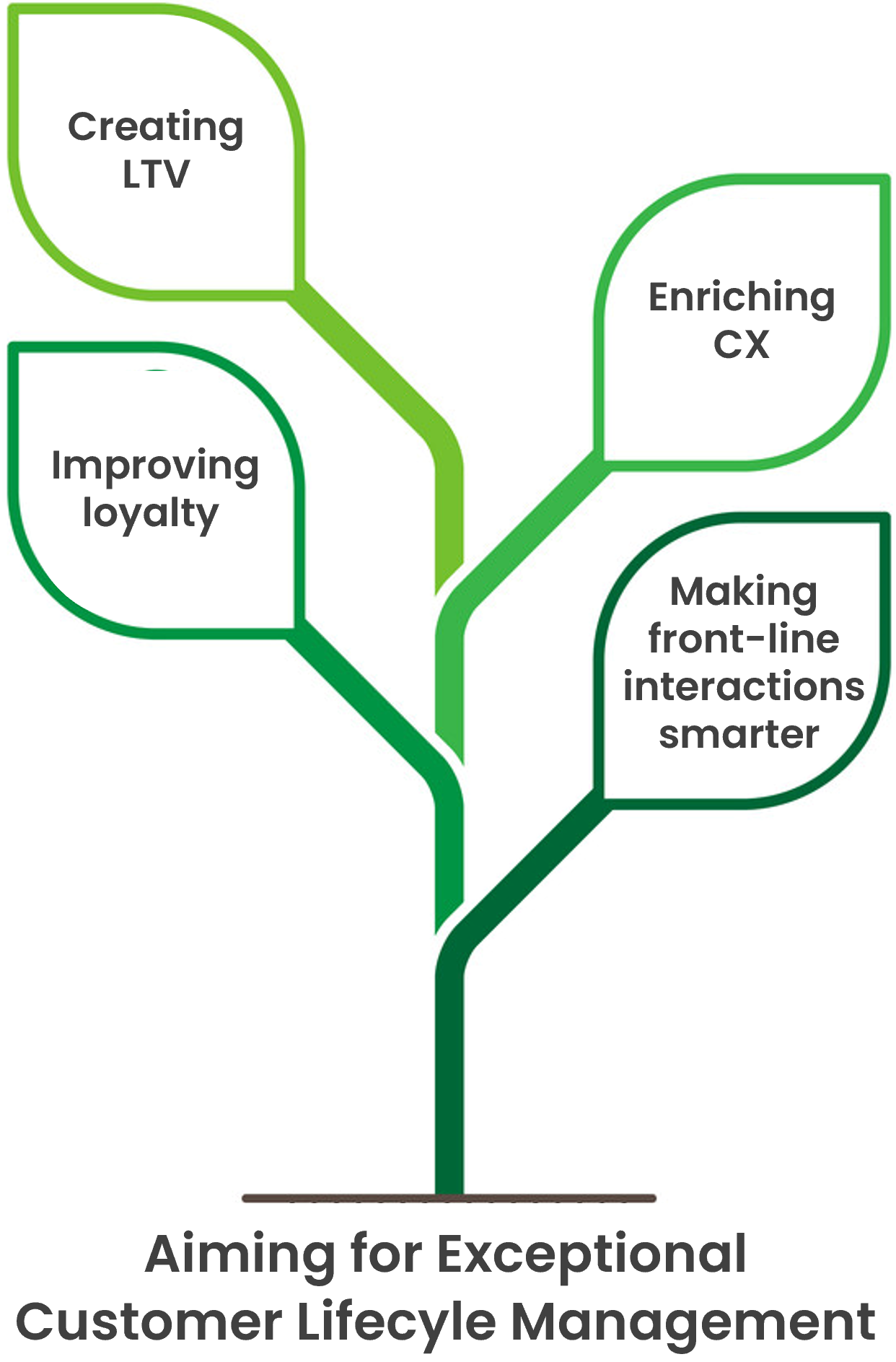

More importantly, it helps FIs enhance the 4 key CLM priorities:

Making front-line interactions smarter

This is an area most FIs struggle with because they strive for absolute real-time, ‘in-the-moment’ insights that are quick and easy to comprehend and actionable. FIs can transform customer-facing staff interactions with real-time insights extracted from deep customer analytics. AI and Machine Learning-led cross-channel customer insight solutions synchronize and synthesize customer intel from across the enterprise and deliver actionable ‘essence’ to the front-line in real-time.

Improving loyalty

Some of the retention challenges financial institutions face include poor metrics on attrition and the lack of an enterprise-wide unified view of the customer. Most financial institutions reactively try to hold on to customers, versus taking a proactive approach before customers decide to leave. FIs can build integrated, cross-functional programs with an in-depth understanding of affinity and traction in relation to new and existing customers. Real-time insights help financial institutions create and monetize customer loyalty programs faster and fine-tune program features to maximize ROI.

Enriching CX

Great CX is a good blend of robust processes, analytics-driven real-time interventions and an exceptional service culture. A CX framework that dovetails with the larger business strategy enables delivering quantifiable value. From price to the product to service, financial institutions can evaluate key customer interaction touchpoints to determine the right experience level to provide, based on a combination of customer expectations and the relative value of each customer.

Creating lifetime value

Financial institutions accumulate enormous volumes of disparate and new sources of data and have the power to achieve the proverbial 360-degree view of the customer. Specialized solutions with the support of deep-analytics and access to relevant contextual insights that help monetize upsell / cross-sell opportunities help deliver significant and sustainable impact.

From acquiring to onboarding to strengthening relationships to growing upsell / cross-sell revenues, while complying with regulatory norms, a sustained, superlative and diligent CLM helps FIs traverse an exciting journey that is not just begun well but also advanced well.

De-risking Onboarding with Cross-channel, Real-time Customer Due Diligence

New IBM configurations designed for flexibility, sustainability and security within the data center

We are excited to collaborate with IBM as the company today unveils its new IBM z16 and LinuxONE Rockhopper 4 single frame and rack mount models available globally on May 17, 2023. Powered by the IBM Telum processor, these new configurations are designed for highly efficient data centers with sustainability in mind. Clients can make more effective use of their data center space while remaining resilient in the midst of ongoing global uncertainty.

Fraud monitoring and prevention is an integral part of banking, needed to protect its customers and business alike. Being compliant to regulatory and market demands is mandatory for banks to function worldwide. With the growing incidence of banking fraud and its societal impact banks have a pivotal role in maintaining the trust of its customers. Globally fraudulent transactions are finding new paths every other day, and banks have to be a step ahead to monitor and prevent them.

Clari5 Enterprise Fraud Risk Management (EFM) solution needs to be responsive in real-time for decisioning. The new IBM z16 and LinuxONE Rockhopper 4 configurations offer scalability on demand with a relatively small footprint. The sytems will support Clari5 to help keep seamless operations running at the bank. Clari5 EFM has to monitor transactions for fraud, and it has to be challenged or stopped in real time. As the volume of business grows or occasional spikes in transaction volumes, the IBM systems provide seven 9s (99.99999%) availability and scalability on demand for Clari5 to continue to monitor and prevent frauds without business disruption.

Clari5’s AI/ML models leverage IBM’s Telum processor to process huge volumes of data to reduce false positives and help in customer onboarding. ML models grow better with growing data elements, and the specialized Telum processor will provide for the much-needed processing power for decisioning in real-time.

Addressing today’s changing IT landscape

Every day, clients face challenges in delivering integrated digital services. According to IBM’s recent IBM Transformation Index report, security, managing complex environments, and regulatory compliance were cited as challenges to integrating workloads in a hybrid cloud. In today’s evolving IT landscape, it can be difficult for clients to meet business objectives while adhering to environmental regulations and increasing costs.

The new rack mount option is designed with the same reliability standards as all IBM z16 and LinuxONE systems and is for client-owned data center racks and power distribution units. This footprint is architected to let companies co-locate the latest x16 and LinuxONE Rockhopper 4 technology with distributed infrastructure and opens opportunities to include storage, SAN, and switches in one frame, designed to optimize both data center planning and latency for specific computing projects. Installing these systems in the data center can help create a new class of use cases, including data center design, optimized edge computing, and data sovereignty for regulated industries.

Securing data on a highly available system

According to IBM’s Cost of a Data Breach report, conducted independently by Ponemon Institute, and sponsored, analyzed and published by IBM Security, surveyed organizations with a hybrid cloud model had lower average data breach costs, about $3.8 million, compared to public or private cloud models. IBM z16 and LinuxONE systems help support a secured, available hybrid IT environment critical to customer outcomes for essential industries like healthcare, financial services, government, and insurance.

More sophisticated cyber threats require new standards of protection. IBM z16 and LinuxONE provide high levels of resiliency offering support for mission-critical workloads. These high availability levels help banks maintain access to data from their customers’ bank accounts, transactions and other personal information whenever they need it. IBM z16 and LinuxONE Rockhopper 4 single frame and rack mount systems offer a broad range of security capabilities, including confidential computing, centralized key management, and quantum-safe cryptography.

Optimizing flexibility and sustainability

IBM z16 and LinuxONE Rockhopper 4 single frame models are built to help maximize flexibility and sustainability in data centers. With a new partition-level power monitoring capability and additional environmental metrics, these single frame systems are dedicated to helping clients reach their sustainability goals, reducing data center space and energy consumption. These key advantages distinguish the platforms for sustainability in the data center, especially when consolidating workloads from x86 servers.

As a part of the IBM Ecosystem, Clari5 is helping companies unlock the value of their infrastructure investments by implementing the tools and technologies designed to help them succeed in a hybrid cloud world. We are excited to be working closely with the IBM Ecosystem to bring new innovations to our clients.

Additional information:

1 March, 2023 | Manila

With a focus on financial inclusion and security, The Ultimate Fintech Forum focused on how digitalization is paving the way for financial inclusion in the Philippines. Rivi Varghese, Founder – CEO, Clari5 shared experiential insights on “How To Make Your Bank Go Higher, Faster, Stronger”.

22-23 November, 2022 | Manila

The flagship event of FintechAlliance.ph, INDX 2.0 FinTech Summit brought together industry leaders, practitioners, and government partners involved in digital finance, digital transformation, innovation, and strategy. With the theme, “The Future of Digital Economy in the Philippines: Issues, Impact and Innovation”, the event highlighted key learnings and solutions in line with national digital initiatives. Jayaprakash Kavala, Chief Products Officer, Clari5 explained how a unified approach to real-time fraud risk Management + AML compliance can be a force multiplier in combating financial crime in banks.

(First in the two-part series on improving Customer Lifecycle Management in banks)

Image courtesy: @snowing on Freepik

Image courtesy: @snowing on Freepik

‘A 1000-mile journey begins with a single step.’

– Lao Tzsu

In a fiercely competitive environment, banks have been striving to generate more revenues while trying to increase customer stickiness and curtail customer attrition. The scenario has compelled the need for a holistic approach for creating strong customer-centricity – the key aim of great Customer Lifecycle Management (CLM).

Be it transaction banking or wholesale banking or cash management services, customers continue to generate significant fee-based revenue for banks. So a robust CLM is vital for serving corporate, institutional, or individual customers. And given the intense competition to win customer loyalty, especially with increasing mergers and acquisitions, banks are now investing much more in transforming their CLM processes.

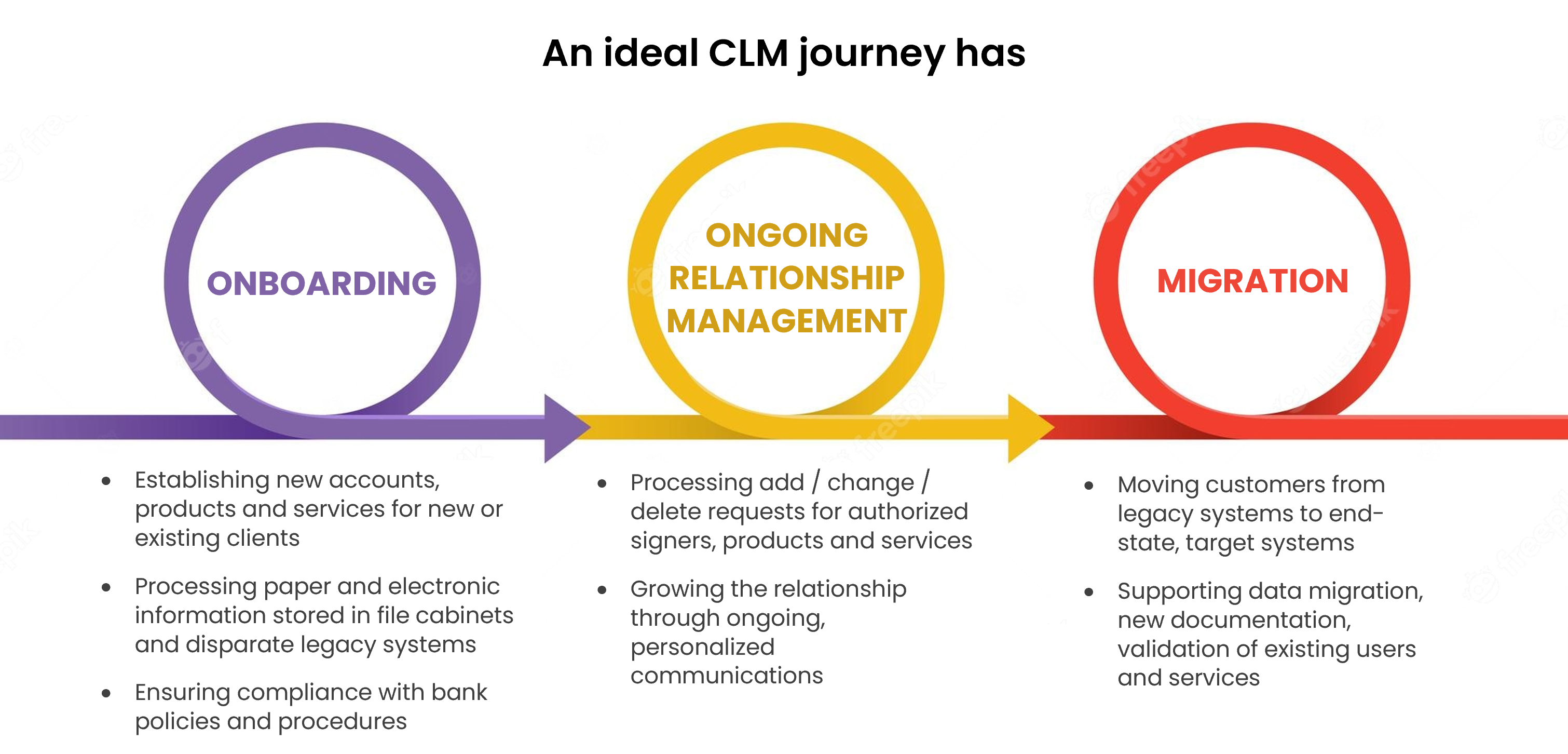

Let’s take a look at step 1 in the CLM journey – Onboarding

Regulatory supervisors around the world are increasingly recognizing the importance of ensuring that banks have adequate controls and procedures in place, so that they know the customers with whom they are dealing. Adequate due diligence on new and existing customers is a key part of these controls. Without this, banks become vulnerable to reputational, operational, legal and concentration risks, which can have significant financial impact.

On the other hand, customers expect convenience, speed + quality of service delivery and personalized service. An efficient Onboarding process reinforces the bank’s customer-centricity while taking care of critical operational risk mitigation procedures such as KYC, Due Diligence, Beneficial Ownership Verification, etc.

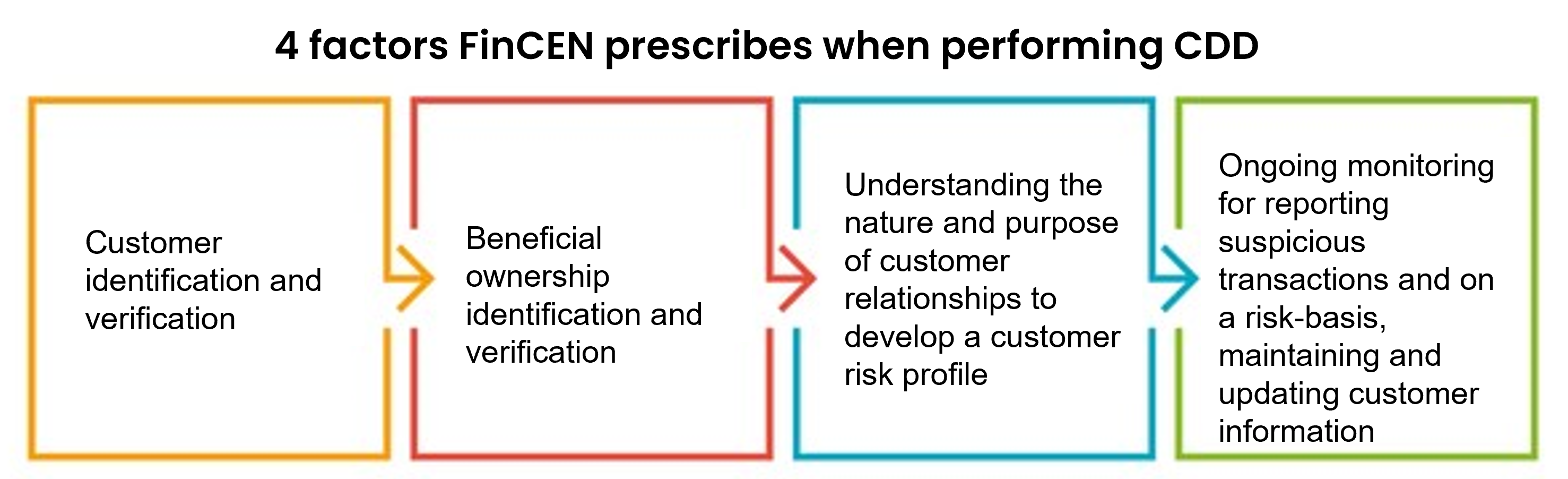

KYC is a critical component in the Onboarding process to help establish the customer’s identity prior to Onboarding and Customer Due Diligence (CDD) is a regulatory norm as part of the KYC process. A bank is required to ascertain the identity of the customer and confirm that funds in the customer account come from legitimate sources.

The first part in a KYC program is a bank’s Customer Identification Program (CIP) which requires collecting and documenting a customer’s name, date of birth, address and identification presented.

The second is Customer Due Diligence (CDD) which requires obtaining information to verify the customer’s identity and assess the risk. If the CDD inquiry leads to a high-risk determination, the bank has to conduct an Enhanced Due Diligence (EDD).

In the US, FinCEN’s CDD rule clarifies and strengthens CDD requirements and requires banks to verify the identity of beneficial owners of legal entity customers.

So, while focusing on delivering a great Onboarding experience, banks must simultaneously ensure and enforce CDD.

CDD helps gauging money laundering risks with a better identification mechanism and mitigates customer-related risks. CRC or Customer Risk Categorization is a risk scoring framework that uses parameters like demographic profiles, geographic, product subscriptions and watch list matches to provide a risk score.

These risk scores are assigned to customers’ profiles during Onboarding and updated along with their journey. Even something as mundane as critical documents expiry updates and notifications, if not handled accurately and on time, can cost banks heavily for non-compliance. In fact, the risk exposure increases when critical information is not updated.

Technology is a key enabler for effective client lifecycle management. There are advanced solutions now available that help banks streamline the complete customer lifecycle assessment and re-assessment of customer risk as part of KYC applicant Onboarding and ongoing CDD processes.

These solutions help streamline money laundering risk assessment, improve understanding of the customer in order to identify, manage and mitigate customer related risks better.

So, what must a bank look for in a good CDD-enabling technology solution?

To determine the relevant risks, 10 key customer information points that banks must collect are:

This is not exhaustive, and banks may need additional information depending on specific facts, but its good enough to start with.

These insights, together with a strong CDD-enabling real-time, cross-channel technology solution can help banks streamline the Onboarding experience as a first step towards a great customer lifecycle journey.

To know how to manage the journey ahead and improve Customer Lifecycle Management in banks, stay tuned for the upcoming part 2 on ‘Enriching the Journey Ahead with Exceptional Customer Lifecycle Management’.

Enriching the Journey Ahead with Exceptional Customer Lifecycle Management